The news of an increasing “medical poverty” was reported shortly after the New Year. Health insurance’s premium collection rate has exceeded 99% since 2010 and the accumulated amount of surplus has reached almost 20 trillion, however, many people still have difficulty in receiving treatment. This is because the current health insurance has some fundamental weak points and it is slow to accept new drugs or techniques of medical treatment. Therefore, the Sungkyun Times (SKT) now provides an overview of medical poverty, its cause of occurrence, and a possible solution to it.

What is Medical Poverty?

Definition

Being “medically poor” refers to a situation where people cannot afford to pay their medical expenses and, in some cases, need to sell their house or borrow money in order to receive treatment. In other words, medically poor people have economic difficulties due to the payment of their medical bills. The major reasons for these enormous expenses are normally due to severe diseases such as cancer or chronic diseases such as diabetes. According to Statistics Korea, over 30% of Korean people give up receiving treatment because of their inability to pay medical bills. About 300,000 of these people have had to sell or move out of their properties in order to continue their treatment. A report released by the Korea Institute for Health and Social Affairs said that the risk of poverty is 1432 times higher for a family in this situation.

Examples

A recent case of medical poverty was of a patient of stage 4 lung cancer, Lee Sung-Mok, who was included in a report on KBS news on January 18. His family sold their house of 30 years to receive treatment for a new anticancer drug which cost 3.4 million and his medical bill came to 20 million in just four months. He could not forgo the treatment of the new drugs because it was reducing his cancer cells by 20%, even though its price was unusually high. His family, however, could not afford the price of these drugs because there was no other support system in place. This case was a good example of where patients started to fall into poverty after selling their property or borrowing money to pay for their healthcare.

Another representative case of medical poverty is ‘The Case of the Mother and Her Two Daughters in Songpa’. A Mother and her two daughters, who lived in Songpa-gu, Seoul, suffered from the hardships of life and finally committed suicide together in February 2014. They were already in huge debt because the father had left them in debt while trying to cure his bladder cancer 12 years before. To make matters worse, the oldest daughter also had high blood pressure and diabetes, but she could not get proper medical care because they could not afford it. The problem was that they had insufficient points to qualify for medical benefits since the mother’s income, 1.5 million, was a little over the minimum required for a family of three to live on. Therefore, they were caught in a blind spot of the health insurance system, despite still paying a monthly premium of 49,000. This was a typical case of a low-income family being unable to afford their medical expenses due to their original economic difficulties.

How has Medical Poverty Emerged?

The Korean health insurance system was good enough to be praised by President Obama as almost 97% of Korean citizens have it and benefit from improved access to health care. In addition, it has remained almost unchanged for 40 years since being established in 1977, due to its excellence. The result of the survey conducted by the Health Insurance Review and Assessment Service last year, however, showed that 13.6% of the 400 surveyed people were afraid of getting cancer and the biggest reason for this concern was due to “medical expenses”. 37% of cancer patients also chose economic reasons as the primary reason for their hardship. This is because there are several problems with the existent Korean health insurance system.

Absence of Accident and Sickness Benefits

Accident and sickness benefits are the extra payments received by people who cannot work during their treatment or hospitalization, in order to compensate for their loss of earnings. Most Organization for Economic Cooperation and Development (OECD)-member countries include these benefits in the form of health insurance or public health security, however, Korea only compensates occupational-related illnesses or those caused by industrial accidents. This can cause people to lose their jobs if they become seriously ill and experience both income loss and burden from medical expenses. These kinds of people are more likely to default their premiums and the current health insurance system limits insurance coverage for people who fail to pay their premium for six months straight. There has been no improvement on this problem, despite the National Human Rights Commission (NHRC) recommending that Korea provide accident and sickness benefits in 2006.

Failure of Insurance Policies

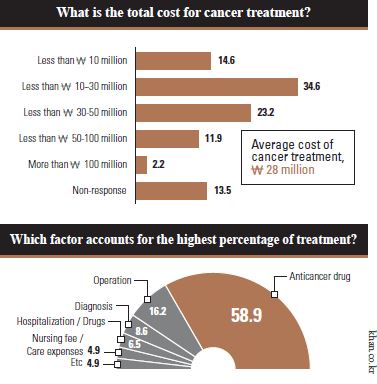

Korea’s National Health Insurance Policies have a problem in that they fail to catch up with the rapid advances in the techniques of medical treatment. According to a report released by the Korea Cancer Care Alliance (KCCA), the registration rate of newly licensed drugs was only 27% in Korea while that of OECD member countries was 62%, between the years 2009 to 2014. In addition, the necessary period for registering a new drug in Korea is 601 days, which is 2.5 times longer than that of the OECD members’ average of 245 days. It means that most cancer patients might be required to pay 20 million themselves because 72% of their average medical expense (2.8 million) would not be covered be by the health insurance system. Most patients who have suffered from these enormous expenses are terminally ill cancer patients who desperately need the latest drug treatments. For example, an immuno-oncology treatment called “Keytruda” costs 100 million per year and a breast cancer treatment called “Kadcyla” costs 120 million. This failure to register new treatments faster, has only helped to increase the strain on the medically poor.

Blind Spots in Health Security System

Two million households have not paid their health insurance premium for a period of six straight months in Korea. The problem is that 56.7% of these people fail to pay 50,000 per month and 50,000 of them are young men under the age of 24. The main cause of this problem is that the health insurance premium is imposed without considering real income. According to the National Health Insurance Corporation (NHIC), 95% of the imposed insurance premium is considered by age, gender, property, and key money for rental housing without income. Furthermore, minors should pay their parents’ premium arrears. A revised health insurance law eliminated the minors’ duty to pay, however, a minor who has a regular income or is single, is still required to pay the overdue premium. The need to consider these disadvantaged groups is growing, but the rate of guaranteeing medical expenses has decreased to 63.2% while that of the average OECD member countries is 80%.

How Should We Handle Medical Poverty?

The Korean Government introduced “Support Businesses of Catastrophic Health Expenditure for Severe Diseases” in 2013 to eliminate blind spots in the health system. It mainly supported low-income people in up to 20 million of their medical expenses. Its payment, however, was suspended due to a lack of finances since it drew money from lottery funds and the Community Chest of Korea. This project temporarily ran until last December, and ended up having to pay 12 billion to medical institutions. This suggests that Korea needs to solve the fundamental problems of the health security system by introducing a permanent system.

Sweden’s National Health Service

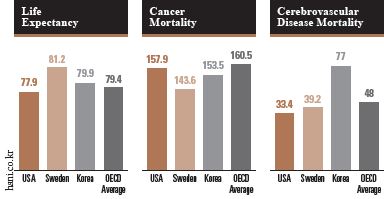

Sweden is famous for having one of the best healthcare systems, through its National Health Service (NHS), in the world. It provides equal medical services to people who live in Sweden regardless of their nationality or economic status. It helps patients to reduce the financial burden of serious illness because it is financed through 71% of local taxes, 16% of government subsidies, and a 3% charge to the patient. Moreover, it includes accident and sickness benefits that secure 80% of income when people cannot work because of their illness. These benefits are funded by taxes, employers, and business workers and are provided to patients through the Social Insurance Agency. In the case of long-term sick leave, the Swedish NHS provides an active rehabilitation program and encourages people to go back to work again after recovery. In addition to this, the NHS has the “0-7-90-90” care guarantee to reduce waiting times of patients with chronic diseases. It requires primary care to be carried out immediately, a general physical examination within 7 days, specialized diagnosis and treatment within 90 days, and an operation within the following 90 days. As a result, Sweden has a higher life expectancy and lower rates of deaths caused by severe diseases, than the average OECD member countries and Korea.

OECD’s Accident and Sickness Benefits

In 1952, the International Labor Organization (ILO) established minimum standards of social security such as medical treatment, diseases, unemployment, and industrial accident at the International Labor Conference. One of the articles obliges countries to pay wages for all illnesses without asking and most OECD member countries except Korea has accident and sickness benefits that follow this article. Taiwan, although not an OECD member country, also introduced accident and sickness benefits recently.

In the case of Germany, this benefit is aimed at people who have lost the ability to work due to serious illness or hospitalization and for those who are required to care for a child with serious illness or disability, under the age of twelve. Support is provided in the form of cash benefits and guarantees 70% of earned income and a maximum of € 94.5 per day. Additionally, France strictly defines people who can benefit from accident and sickness benefit. For instance, they should be insured for at least the last 12 months and should have worked at least 800 hours during that period. When people satisfy these specific requirements and cannot work due to their illnesses, benefits will be provided for a maximum of 360 days, over a three year period. In the case of long-term disease, it will be continuously provided for three years. It really helps patients to support themselves since it ensures income from 50% to 66%. Therefore, Korea needs to introduce accident and sickness benefits to the healthcare system as other countries’ cases have already established the positive effect of these benefits.

The reason why people consistently discuss the improvement of the National Health Service is that the health of citizens is closely related to national power. In other words, a country can grow and develop when the people stay healthy through its healthcare service. In this respect, the news of an increase in medical poverty is a reality to cause worry. A Korean National Health Service, however, would rapidly resolve this problem by closing some of the loopholes and relieving a massive burden from those who desperately need care, but cannot afford it.