zero-pay, a simple payment service introduced by the government as a trial service last December, will be officially launched in Seoul from May. Zero-pay, one example of a simple payment service that uses Quick Response Code (QR code) in a smartphone, reduces payment commission to zero percent by directly transferring between consumers and sellers and minimizing the involvement of the brokerage agency. Currently, despite the government’s promotion for the activation of Zero-pay, not many merchants use the service and few consumers are aware of the service. Nonetheless, Zero-pay continues to be more easily available in daily life due to those strengthened promotions. Accordingly, the Sungkyun Times (SKT) now explains how to use Zero-pay, its expected effects, the potential concerns, and positive prospects.

What Is Zero-pay?

The Background on Adoption of Zero-pay

Zero-pay is a QR code based simple payment system adopted by the government, Seoul City, local governments and private companies of simple payment services. It can make payment easier by using QR codes without using existing credit card payment networks. It was adopted to ease the rising burden on small business owners who have suffered from the increase in the minimum wage. A small business owner refers to business owners who have less than five permanent employees. Exceptionally, the criterion for the number of employees working for construction, mining, transportation, and manufacturing businesses, is ten. With Zero-pay, the government is looking to substantially improve the economic situation of small business owners by lowering the pay transaction fee to the zero percent level, which previously accounted for half to two-thirds of their profits.

How Consumers Use Zero-pay

Basically, Zero-pay is a mobile direct payment system that transfers money from a consumer’s banking account to a merchant’s account when a user scans a QR code with a smartphone application. There are two ways to use this payment. One way is the Merchant Presented Mode (MPM) where a consumer pays by scanning a QR code provided by the merchant through a mobile easy payment application. The other way is the Customer Presented Mode (CPM) where the payment is made when the merchant scans the QR code on the consumer’s payment app. Currently, CPM is being tested in 26 franchises, including BHC and Paris Croissant, and the government plans to increase the number of MPM-enabled merchants. In order to use Zero-pay, consumers do not need a separate Zero-pay application. Consumers can use the existing mobile banking applications and other simple payment apps that provide a QR code function for Zero-pay. In other words, the Zero-pay function has been updated on the existing applications. Currently, about 20 banks, including Shinhan Bank and Woori Bank, as well as 27 simple payment companies such as PAYCO, provide a Zero-pay service. If consumers already have a bank application installed, then money can be transferred directly from their bank account. Also, if they have a simple payment application, all they have to do is to link their bank account to the payment app, and then the transfer takes place. The government also plans to adopt the Near Field Communication (NFC) payment method, depending on the characteristics and demands of each store. Using NFC, payments will be much easier just by consumers getting close to the NFC terminal with their smartphones.

Current Status of Zero-pay

Since the first trial adoption in Seoul, Zero-pay has now been extended to several other regions. Gyeonggi-do, Gyeongsangnam-do, Busan, and Daegu also plan to adopt Zero-pay to keep up with the trend. Furthermore, six big convenience stores, including CU and E-Mart 24, plan to adopt Zero-pay by April. In spite of the government’s great efforts to hype it up, Zero-pay’s performance is currently quite poor. According to a survey of 600 residents of Seoul City conducted by the Korean Foodservice Industry Research Institute (K-FIRI) in March, more than half (67%) of consumers consider Zero-pay as positive, and only 59% are willing to use it. Ironically, the actual situation is not that good. According to the Zero-pay payment status data from the Financial Supervisory Service, Zero-pay facilitated 8,633 payments with the total amount of only 199.49 million won in January, which is less than one-fiftieth of 9.8 billion won, the promotional budget for Zero-pay in 2019. Besides, this was only 0.0004% of the total number of payments made through personal credit and check cards in the same period, which was 58.1 trillion won.

Concerns About Zero-pay

Immature Infrastructure

Zero-pay is currently facing considerable difficulties in increasing the usage rate, and experts say that the biggest factor of this is the immature infrastructure. Due to the government’s lack of promotion, many people still do not know about how to use Zero-pay and its benefits, and only a few merchants use it. The data of January from the Ministry of SMEs and Startups shows that only 40,628 merchants officially adopted Zero-pay in Seoul, which is less than 10% of the number of small business stores in Seoul. It means that, even if consumers want to pay with Zero-pay, they cannot use it because there are not many merchants who have adopted the system. The government needs to map out specific plans to solve these problems of the shortage of Zero-pay’s supply.

Inferior Benefits to Existing Credit Cards

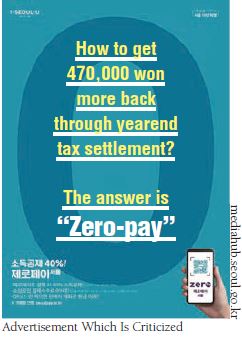

In addition to Zero-pay’s lack of infrastructure, it is not effective enough to change the credit card payment habits which are currently used by most people. These days, most consumers are so used to paying with credit cards. Moreover, many credit card companies offer consumers a variety of benefits such as interest-free installment payments, discounts on telecommunication fees, and air mileage savings. Therefore, for Zero-pay to be well activated, it is necessary to give more benefits to attract consumers to use Zero-pay, giving up the benefits of credit card. Besides this, there are some loopholes in the advertisement phrase of Zero-pay, saying that “You can get 470,000 won more back through year-end tax settlement”. The advertisement says that if they use half of their salary with Zero-pay, consumers with an annual salary of 50 million won can get back 470,000 won more compared to the credit card. This is, however, not quite realistic. First, it is unrealistic to spend more than 2 million won in a month only with Zero-pay payment. Second, for 470,000 won higher tax deduction, the current limit of the amount deducted from one’s income tax must be increased from 3 million won to 5 million won. In other words, unless the current tax exemption regulation law is amended, the benefits of 40% deduction of income tax would not be valid. Currently, the Democratic Party has proposed an amendment to the law that it might be revised this year. Nevertheless, it is argued that promoting before the final amendment of the law is an exaggerated advertisement.

Misuse of the People’s Taxes

The public sector exists for public well-being and is run off of the taxes of the people. Some argue that it is undesirable for the government, the public sector, to violate and compete against the private financial sector using taxes. Zero-pay is a new competitor in the payment service market that causes competition between the government and the credit card companies, a private sector formed over a long period of time. As a result of the government’s pressure to cut card payment fees, the net profit of eight card companies including Samsung Card and Hyundai Card dropped to 32%. If Zero-pay, which has no payment fees, is used around the country, it is expected to pose a greater threat to credit card companies which make the most profits through card payment fees. As a result, there is an argument that the credit card companies are sacrificial victims for the government’s policy stunts.

Benefits and Prospects of Zero-pay

Although Zero-pay is still in the early stages of adoption, which brings concerns, it has many benefits.

Benefits for Business Owners (Sellers)

Zero-pay can ease the burden of small business owners by lowering the rate of payment commission to 0-0.5%. Based on the previous year’s revenue, the commission is 0% for those who earn less than 800 million won, 0.3% for those whose annual sales are between 800 million won to 1.2 billion won, and 0.5% for those who exceed 1.2 billion won. This is a very low degree compared to the 1.6%, which is the highest commission rate of credit cards for those who earn less than 3 billion won. According to Statistic Korea, 96.8% of restaurants in Korea earn less than 1 billion won a year. This means that Zero-pay will be a significant help to small business owners. Besides this, they can also easily manage their store’s payment status in real time with Zero-pay websites and applications.

Benefits for Consumers

Zero-pay does not only ease the burden of merchants but also benefits consumers. From 2019, Zero-pay offers a much higher income deduction rate. Consumers can get 40% deduction when they use Zero-pay in small business owner’s stores, which is much higher than the deduction rate of credit cards (15%). Since, the government continues to reduce the deduction rate of credit cards nowadays, Zero-pay with a high deduction rate can be a great benefit to consumers. In addition, there are also discount events for public facilities including parking lots and cultural facilities. Currently, there are 10%-30% discounts on the admission fees of the Sejong Center and the Seoul Philharmonic Orchestra’s performance tickets. Moreover, from April to May, these benefits will expand to about 390 public cultural facilities in Seoul, including the Children’s Grand Park. Besides, since March, Seoul City has introduced a policy to return 1%-2% of spending to T-mileage when paying with Zero-pay through the mobile T-money application. With T-mileage, consumers not only can charge their T-money, but also can convert it to cash when a certain amount of mileage is accumulated, which is the same as the cash-back of credit cards. Furthermore, the government is considering ways to pay apartment management fees, electricity and local taxes with Zero-pay.

Zero-pay, which started with good intentions to ease the burden of small business owners, is not welcomed yet by both merchants and consumers. Some people even cynically say that the number of consumers who use Zero-pay is Zero. In order for Zero-pay to become a system that can benefit both sellers and consumers, the current problems of Zero-pay need to be solved by considering the users’ point of view and increasing their convenience.