According to a survey in 2017 conducted on a part-time job recruiting website, the average monthly cost of living for university students was 690,000 won. Also, six out of every 10 college students have said that they work parttime jobs along with their school study, so it seems that parttime jobs are now an inevitable choice for young people in need of living expenses. The student living expenses loan is a system designed for university students who tend to earn less but spend more. The Sungkyun Times(SKT) decided to find out about loans for university students which are like a double-edged sword.

About the Student Living Expenses Loan

The student living expenses loan is for young people who are unable to concentrate on studying and have to prepare for jobs due to the cost of living. It provides loans at low interest rates of between 2 to 5 percent and is set for the students to pay back the loans when they are able to pay them. This system is very convenient for university students, considering that there are barely any bank loans that college students can borrow. There are some loan products for jobless youths but the interest rates range from 10 to 20 percent which is still very high.

Three projects publicly support loans for college students: student loans (living expenses) from the Korea Student Aid Foundation (KOSAF), Sunshine loans, and the Happy Fund. KOSAF’s student loans (living expenses) is the most used program by students. The Sunshine loan offers lowinterest loans for the young and university students. The Korea Asset Management Corporation (KAMCO) supports the Happy Fund that can ease the burden on college students and young people who take out loans with high-interest rates for living funds.

Problems of the Student Living Expenses Loan

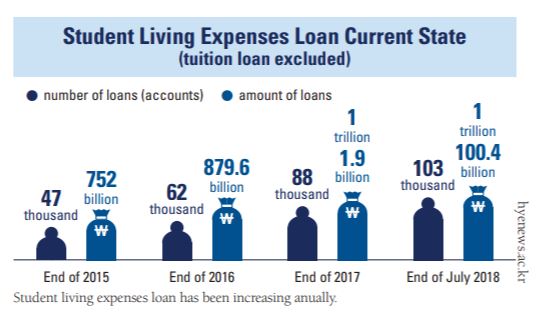

Young People Taking First Steps into Society with a Pile of Debt

Young people are taking their first steps into society with great debt, since getting a job is so difficult on the contrary to how easy it is to borrow money. The amount of overdue loans is increasing at a greater rate compared to the increase in the college student living expenses loan. In fact, the number of young people who are six months behind on general repayment loans currently stands at 11,649, and the number of unpaid loans for post-employment loans has also increased every year to 25,070 last year. Although the youth debt problem is not being treated as seriously as household debt, the nation’s youth debt problem will become much more serious in the long run.

Oversimplified Loan Procedure

In a way, an overly simple procedure may seem like an advantage. However, it holds a fatal drawback. Critics say that the student living expenses loan procedure is too simple in that it encourages young students to borrow money. The KOSAF’s after-employment cost-of-living loans only assess income distribution, but credit requirements are not subject to evaluation at all. The loan procedure is to watch eLearning videos, enter bank account information, and execute the loan on the website. Afterwards, the money is deposited directly into the account right away. Unlike how it seems convenient to lend money from KOSAF, it has got its dark side when it comes to repayment. It is notable that the loan by the KOSAF also has a credit crunch caused by the loan, which is not much different from that of other financial institutions. Student living expenses loans could also reduce credit ratings and degenerate into credit delinquency.

Direction of Student Living Expenses Loans

Strengthening the Government’s Welfare Policies

In order to reduce the burden of living expenses for college students, school or national measures are needed. The government should increase support for housing costs, a part of students’ heavy burden on living expenses. It is inevitable that most young students would have to put their hands on the cost of living loans because it is too much to earn while going to school. Also, solving the employment difficulties of young people will be a powerful solution. As the problem is that it is easy to borrow but not easy to pay back, the government should improve self-reliance to help ease the employment shortage among young people.

Suitable Procedures for University Students

As the student living expenses loan is a product for college students and young people, loan procedures should be changed to take into account their characteristics and circumstances in the process. College students lack economic management skills due to a lack of social experience. Therefore, the practical solution is to add counseling procedures to the college student and the cost-of-living loan process. From the time a young student tries to borrow money, the actual lending procedure should be followed by systematic counseling on what it means to get a loan and why he or she is in debt. While the loan process can become cumbersome when the consultation process is added, it can make the responsibility of getting loans more visible and increase understanding to reduce loans that will lead to unnecessary debt.

University students are stuck somewhere in the middle; not the adolescents under parents’ and schools’ rooves, not the office workers who build careers in society and run for a better life. Everyone says it’s the best time of life, but the reality is harsh. Strangely, the money earned is small, but the money spent is large. At this point in time, the growing debt of youth is considered to be as serious as household debt. Youth debt is no longer just a matter for young people, so the government financial organizations and universities should form a consultative body to find a solution.