Most of us might have used a simple payment service such as Toss or Kakaopay at least once. The simple payment service is a convenient service that people of all ages like to use. Since the government announced that Open Banking is completely employed this December, the service market is expected to grow more rapidly. Therefore, the Sungkyun Times (SKT) is going to look at the simple payment service, its problems, and ways for improvement.

About Simple Payment Services

Definition and Development Status

The simple payment service is a service in which the user can send money through his or her mobile device without using a public certificate or One Time Password (OTP) card. If the procedure of authenticating with one of your public certificates, Advanced Record Systems (ARS), and the message is done when a user signs up for an account, one can send money only with his or her short password after this. In March 2015, the government loosened financial transaction security regulations by taking measures such as abolition mandatory public certificates. As a result, the simple payment service market began to grow. After the fintech company Viva Republica provided the service through its mobile app Toss for the first time in Korea in February 2015, other fintech companies like Naver and Kakaopay began to enter the market. A fintech company is a company that provides a service that combines finance and technologies. In 2018, seven fintech corporations provided simple payment services in Korea: Viva Republica’s Toss, Naver’s Naverpay, Kakaopay’s Kakaopay, Coocon’s Checkpay, NHN PAYCO’s PAYCO, LG U+’s Paynow, and Finnq’s SK Pay. Thanks to these convenient services, both the number of transactions and the amount of money traded have been increasing rapidly. According to the Bank of Korea, the average number of transactions per day in 2018 was about 1.4 million, and it had grown by 100 percent compared to the previous year. The amount of money traded per day in 2018 was about 104 billion, and this number doubled since 2017.

Defects of the Simple Payment Service

Weak Profit Model

Most fintech corporations provide simple payment services for free to gather users and gain profit by offering other financial services. For example, Toss makes most of its profit by earning a commission that comes from selling banking institutions’ products. Therefore, the users should not feel assured of corporations’ financial stability with the number of users and the amount of money traded on the market. In fact, most fintech corporations are deep in the red despite the fast growth of the market. Even Toss, which has a leading position in the industry, has an accumulated deficit of over 100 billion won over the past three years. This is because they should pay a large number of remittance charges to banks. The average remittance charge per transaction is about 150 to 450 won, and it is a colossal amount of money considering the number of transactions traded per day.

Strict Financial Regulations

In Korea, corporations can launch the service when financial authorities allow and specify the rules related to that. This means that if related regulations do not exist in Finance Acts, the service cannot be introduced regardless of its innovativeness and convenience. For instance, when Toss was released, it was in danger of being branded as an illegal service because there were no regulations covering its innovative technology. However, it could be released safely since the Financial Services Commission recognized Toss’s innovativeness and modified the financial laws. Nevertheless, it is spending a lot of time and money in revising the law whenever an innovative service is introduced. In the case of Toss, the service wasted about nine months in solving the problem related to regulations. Besides this, strict contents of the regulations create hostile conditions for fintech corporations to grow. It is prohibited for corporate bodies and minors to make financial transactions through fintech corporations online. It makes them use stock firms’ marketing networks. As well as this, they are not allowed to sell their own products, so they just get a commission on the sales of other banks’ products.

Directions for Improvement for the Simple Payment Service

Building Solid Profit Model with Open Banking

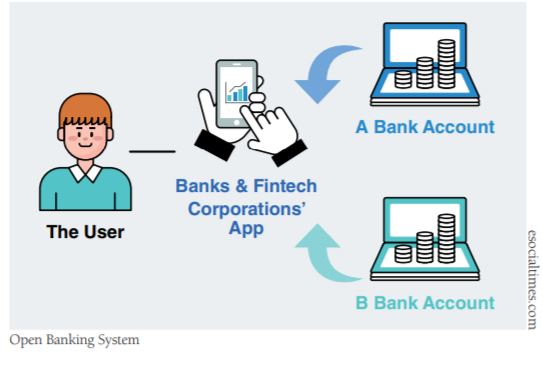

Today, fintech corporations should form an alliance with banks and give remittance charges to use banks’ exclusive payment systems. However, the government stated that Open Banking which allows outsiders to access the financial information of the bank starts from this December. By using Open Banking, fintech corporations can view other banks’ accounts and remit the money on their apps without establishing an alliance with banks at a substantially lower cost. It can reduce remittance charges to a scale of one-tenth of the original amount. Finally, this will lead the corporations to invest their money to improve the service. For example, the CEO of Toss Lee Seung-gun said that they can offer a free remittance service without limitation through Open Banking. The improved service will attract new customers and it will help build a stable profit model.

Alleviating Financial Regulations

Strict financial regulations should be changed since the existing law has obstructed innovative services to enter the market. Specifically, the government should consider specifying prohibited matters and allow the rest to be unspecified. By alleviating strict regulations towards new technologies, it can contribute to the simple payment service market’s development. Also, a regulatory sandbox could help lower the entry barriers for new services. The regulatory sandbox is a system that does not apply the original regulations to new services and helps them enter the market. In 2019, over 20 countries enforce the system, and specifically in the case of the United Kingdom (UK) that started the system for the first time in 2016, 90% of corporations tested in 2016 officially launched their service successfully. A regulatory sandbox can prevent the creative service from falling apart by the traditional regulations. The change in this way will accelerate the development of the simple payment service market, and furthermore, the financial market.