To celebrate World Environment Day on June 5, the Sungkyun Times (SKT) will look at a new active green policy called “climate bond,” or more commonly “green bond,” which replaces the already known eco-friendly policies such as the emission trading scheme and the carbon tax. Green bonds have already been actively issued abroad, but their appearance in Korea has been very gradual. The SKT attempts to explain green bonds and the aspects of its position in the Korean market, as well as its significance and limitations.

What is a Green Bond?

Concept

A bond in itself is an investment debt with a fixed interest rate and maturity date. Bonds can be an effective way for companies to raise funds and for investors to gain stable profits, since investors can receive money back once the maturity date passes. A green bond is a bond that is only issued for special purposes such as bio-energy, sustainable management of waste, biodiversity, efficient energy, or other such climate change solutions. The Center for International Climate and Environment Research (CICERO) examines the eligibility of these special purposes in order to ascertain that the plans made by a company are beneficial to the environment. This process is called the “certification of a climate bond.”

Background

After the agreement on new systems for climate changes were established at the 21st United Nations Framework Convention on Climate Change in 2015, the interest in eco-friendly investment rapidly grew. Furthermore, after the poor performance of the emission trade scheme in Europe and the abolition of the carbon tax in Australia, the necessity for an active method of gathering funds to deal with climate change has increased. Thus, as an active fund, the European Investment Bank began issuing green bonds in 2007 for the first time. In sequence, the World Bank, the African Development Bank Group, and many other institutions issued green bonds. In the initial stages, green bonds did not attract investors due to their low interest rates; however, as the uncertainty of the world economy increased, the green bond market started to receive attention as a long term investment market.

Advantages

Today, more and more institutions are releasing green bonds due to their advantages. From the issuer’s perspective, the green bond helps issuers gain specific investors whose sole interest lies in eco-friendly industries, which broadens the range of investors. Issuers can also improve their company image by emphasizing their commitment to the environment. From the investor’s perspective, they can participate in high-risk environmental investment through the relatively stable method of green bonds. The green bond initiates thoughts about eco-friendliness for both consumers and producers. The green bond market is growing rapidly, and with this growth, the green bond can reinforce companies’ social responsibilities as well.

Owing to these advantages, the green bond market is already being called a “$100 billion market,” and many companies are willing to participate in it. This year, for example, Apple participated in the green bond market by providing $1.5 billion worth of green bonds to establish eco-friendly office buildings, data centers, and bio-energy industries. Additionally, FlexiGroup, a financial service business based in Australia, issued an impressive green bond initiative to provide cheaper rooftop solar panels. There is an active investment in and issuance of green bonds taking place around the world.

Green Bonds in Korea

In Korea, however, a green bond is still a rather unfamiliar term, and the issuance of and investment in green bonds has hardly been achieved. The Export-Import Bank of Korea published green bonds only twice, in 2013 and 2016. The reason for this is that the green bond market is not an active market, and the economic and political situations of Korea have hindered the green bond market from establishing a foothold in the Korean market. To further explain the economic issues, many private companies in Korea do not consider environmental sustainability as their first priority, while many foreign companies maintain eco-friendly economic management. Thus, private Korean companies face difficulties in passing CICERO’s standards for the certification of climate bonds, which require companies to follow international environmental rules set by the OECD. As for Korea’s political situation, this mainly comes down to the fact that Korea is a divided nation-state. North and South Korea are under suspension of fire and constant tension. Therefore, when North Korea pushed a nuclear experiment, there was a risk of lowering South Korea’s credit rating, which then led to a decrease in investors. Mostly, the uncertainty of gaining investors was the main reason for the inactive issuance of green bonds in Korea.

With these concerns, the Export-Import Bank of Korea issued the first green bond in 2013 to support the eco-friendly project of “low-carbon and climate resilient growth.” The Export-Import Bank passed CICERO’s standards with good scores. Moreover, when the voice of concern roared due to North Korean nuclear experiments, international credit rating institutions stilled the global atmosphere by insisting that North Korea would not affect South Korean economic fundamentals (basic standards that show a country’s economic state). In fact, North Korean nuclear experiments did not affect the South Korean economy, which led to the successful issuance of Korea’s first green bonds.

Since the Korean green bond had an interest rate that was 0.95 percentage points higher than the national bond of the United States (US), it attracted many American investors. As international credit rating institutions raised the Korean credit rating from A to AA, the number of investors for the Export-Import Bank of Korea increased three times as much as the number of green bonds available in the market. Due to their first success, the second issuance of green bonds by the Export-Import Bank of Korea was effectively implemented in February 2016.

There are also private companies that attempt to publish green bonds. For example, in March this year, Hyundai Capital successfully issued green bonds, which was the first time a private company was able to do so. Hyundai planned to use these funds for marketing hybrid and eco-friendly cars. Therefore, it can be said that the green bond market in Korea is certainly growing.

Significance and Problems

Significance

The green bond is an active policy to raise funds for eco-friendly projects. Normally, it is difficult to raise enough funding for eco-friendly projects because they require building new infrastructures and consume significant time and money. For these reasons, investors who are seeking to gain as much profit as possible in a short period of time usually refuse to invest in eco-friendly

projects. However, with the implementation of the green bond,

issuers can effectively attract investors because the concept of

bond itself is designed to raise funds in the long run.

Furthermore, since most green bonds are very similar to national

bonds and are issued by highly respected credit institutions, investors

can more actively and safely buy green bonds. The green bond has

low risks due to its fixed interest rate and fixed maturity date. These

qualities attract investors who also have good credit ratings.

Additionally, green bonds support companies’ sustainable growth

and can be an effective financial policy for national export-import

banks to support companies. If export-import banks issue green

bonds with low interest rates and prolonged due dates, companies

can actively manage their business while focusing more on ecofriendly

projects.

Problems

On the other hand, the green bond is not perfect. When the green

bond market was still minor and before private companies could

issue green bonds, there was a limit on projects that institutions

could undertake with the funds. With many issuers being high

credit banks, there was little need for third party verification.

However, as more and more private companies participate in

issuing green bonds, their purposes went beyond the maintenance

of the environment and the development of sustainable energy,

reaching into spheres such as marketing and building databases.

This caused ambiguity in the standard to obtain certification as

a climate bond, and it became increasingly difficult to evaluate

a project’s eligibility. In order to prevent abusing green bonds,

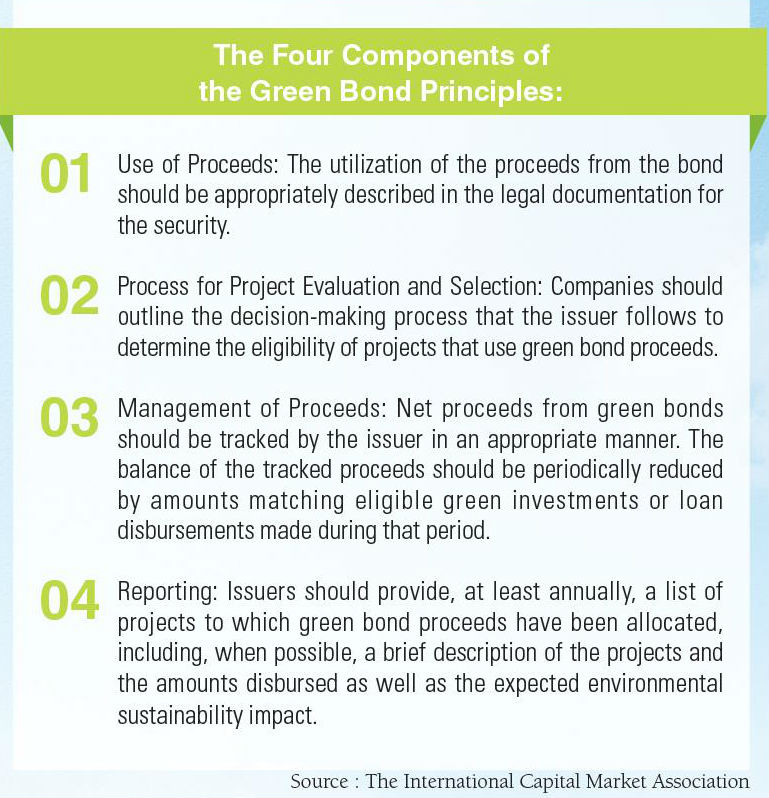

13 international financial institutions, including the Bank of

America Merrill Lynch (BoAML), Citigroup, and JPMorgan Chase,

constructed the “Green Bond Principles” for companies to follow

when issuing green bonds.

However, since the principles were established by mere

international institutions, they lack compulsion, and national

governments have been unable to introduce policies to stop the

abuse of green bonds. These factors bring out the need for a third

party to verify issuance of these green bonds.

The green bond market will expand as time passes. It is growing at a rapid rate, and the green bond will soon emerge as the main method to raise funds for environmental projects. The issuance of green bonds has been very passive in Korea due to economic and political situations. However, as the structure of the Korean economy has become more eco-friendly, Korea is gaining attention as an important market for green bonds. The Bank of America has already mentioned the growth potential of the Asian green bond

market, including that of Korea, as these markets are growing faster than the US and European green bond markets and are still gaining momentum. With the green bond, Korea can take a further step towards eco-friendly industries.